Published: Oct 18, 2024

How to Buy Cheap Renters Insurance Online in 2025

How to Buy Cheap Renters Insurance Online in 2025

I’ve seen more naked apartments than a New York real estate agent… and trust me, you don’t want yours to be stripped bare by a disaster! Let’s cover up those valuables with some dirt-cheap renters insurance, shall we?

TLDR: How can I find the best deal on renters insurance online?

1️⃣ Compare quotes from multiple insurers

Shop around and get quotes from at least 3-5 companies to find the best rates.

2️⃣ Look for discounts and bundling options

Many insurers offer discounts for things like security systems or bundling with auto insurance.

3️⃣ Choose appropriate coverage levels

Only pay for what you need by accurately estimating the value of your belongings.

Table of Contents

- Why You Need Renters Insurance

- What Does Renters Insurance Actually Cover?

- How Much Renters Insurance Do You Really Need?

- Top Picks for Affordable Renters Insurance in 2025

- Tips for Scoring the Cheapest Renters Insurance

- How to Buy Renters Insurance Online: Step-by-Step Guide

- Common Mistakes to Avoid When Buying Renters Insurance

- Frequently Asked Questions About Affordable Renters Insurance

Why You Need Renters Insurance

Picture this nightmare scenario: You’re chillin’ at home when suddenly, your upstairs neighbor’s overflowing bathtub crashes through the ceiling, turning your living room into a swampy mess. 💀 Your laptop, couch, and grandma’s antique lamp? Toast. Without renters insurance, you’re up a certain creek without a paddle…

But wait, doesn’t your landlord’s insurance policy swoop in to save the day? Not so fast, my friend! 🦸♂️ A landlord’s property insurance typically only covers the building itself, not YOUR personal belongings. Yep, you’re on your own when it comes to replacing your water-logged stuff.

Real-Life Horror Stories 🙀

- Remember the 2021 Texas winter storm that caused over $15 billion in insurance losses? Burst pipes wrecked countless rental properties AND tenants’ precious possessions.

- How about the time your buddy’s Renter-Ruining Rover chewed through his entire vinyl record collection? Without liability coverage, he was singin’ the blues. 🎶

Cold, Hard Facts 📊

- Over 60% of renters don’t have insurance, according to the Insurance Information Institute. That’s a whole lotta people gambling with their stuff!

- The average renter owns $35,000 worth of personal property, reports State Farm. Could you afford to replace all that out-of-pocket? 💸

Common Misconceptions Debunked! 🙅♂️

“I’m young and broke, I don’t own anything valuable!”

- WRONG! Your phone, laptop, clothes & furniture add up quick. Plus, liability coverage is clutch if you accidentally damage someone else’s property or injure a guest.

“Disasters won’t happen to me, I’m invincible!”

- NOPE! Theft, fire, and water damage can strike anytime. FBI stats show a burglary occurs every 25.7 seconds in the U.S. 🕵️♀️

“Renters insurance is way too expensive, I can’t afford it!”

- AS IF! The average policy costs just $174 per year, or about 50¢ per day according to the National Association of Insurance Commissioners. That’s less than your daily coffee fix! ☕

So, unless you’ve got a trust fund to burn, renters insurance is a no-brainer. It’s like a superhero cape for your stuff AND your bank account. 🦸♀️ Don’t be caught with your pants down when disaster strikes - suit up with a renters policy ASAP!

What Does Renters Insurance Actually Cover?

Alright, let’s break it down - what exactly is this magical “renters insurance” covering? 🪄 It’s not just a fancy name for your landlord’s policy (which, spoiler alert, doesn’t give a hoot about your stuff). Renters insurance is like a superhero team 🦸♀️🦸♂️ swooping in to save the day when things go sideways.

The Dynamic Trio of Coverage 💪

Personal Property Protection This is the MVP of your policy. It covers your precious belongings from theft, fire, water damage (lookin’ at you, burst pipes), and other disasters. We’re talking everything from your PlayStation 5 to your prized Air Jordan collection. 👟

Liability Coverage

Accidents happen, even to the best of us. If you’re held responsible for damaging someone else’s property or if a guest gets injured at your pad, liability coverage has your back. It can even cover legal fees if you get sued! 👨⚖️

Accidents happen, even to the best of us. If you’re held responsible for damaging someone else’s property or if a guest gets injured at your pad, liability coverage has your back. It can even cover legal fees if you get sued! 👨⚖️Additional Living Expenses (ALE)

If your place becomes uninhabitable due to a covered disaster, ALE steps in to cover temporary housing and extra expenses like food and laundry. It’s like a little vacay while your spot gets fixed up! 🏨

If your place becomes uninhabitable due to a covered disaster, ALE steps in to cover temporary housing and extra expenses like food and laundry. It’s like a little vacay while your spot gets fixed up! 🏨

Real-World Scenarios 🌍

🔥 The Great Apartment Fire of 2023: Your George Foreman Grill goes rogue and starts a kitchen fire. Personal property coverage replaces your charred belongings, while ALE puts you up in a swanky hotel.

🐶 Fido’s Big Oopsie: Your furry friend mistakes your neighbor’s designer shoes for a chew toy. Liability coverage pays for the damages and keeps you out of the doghouse!

💻 The Case of the Vanishing Laptop: Some jerk swipes your MacBook Pro from your local Starbucks. Personal property protection replaces it faster than you can say “grande non-fat latte.” ☕

Mind the Gaps 🧐

Now, renters insurance isn’t a magical cure-all. Most standard policies WON’T cover:

- 🌊 Flood Damage You’ll need separate flood insurance for that. Thanks, Hurricane Katrina!

- 🚗 Car Theft or Damage: That’s what your auto insurance is for, silly goose!

- 💍 Pricey Jewelry, Art, or Collectibles** Got a Rolex or a rare Beanie Baby? You might need extra coverage for those big-ticket items.

So there you have it - the wild, wacky, and wonderful world of renters insurance coverage! 🎉 It’s like a secret weapon for protecting your stuff and your sanity. Don’t be caught with your pants down - make sure you’re covered! 👖

How Much Renters Insurance Do You Really Need?

Alright, so you’ve decided to join the cool kids club and get renters insurance. 😎 But now you’re probably wondering, “How much coverage do I actually need?” 🤔 Don’t worry, we’ve got you covered (pun intended)! 😉

Take Inventory of Your Stuff 📝

First things first, you gotta figure out how much your belongings are worth. And no, “a bajillion dollars” is not an acceptable answer! 💰 Here’s a simple way to calculate your coverage needs:

- Make a list of all your possessions, from your trusty iPhone to your beloved Star Wars action figure collection. 🗒️

- Estimate the value of each item. Pro tip: Use online retailers or eBay to get current prices for similar items. 💸

- Add it all up to get your total personal property value. 🧮

Real-Life Example 🌍

Let’s say your stuff includes:

| Item | Estimated Value |

|---|---|

PlayStation 5  |

$500 |

MacBook Pro  |

$1,200 |

| Clothing and shoes | $3,000 |

| Furniture | $2,500 |

| Other electronics and appliances | $1,500 |

| Total | $8,700 |

In this case, you’d want at least $10,000 in personal property coverage to give yourself a little wiggle room. 🕺

Don’t Forget Liability! ⚖️

Liability coverage protects you if you’re held responsible for injuries or property damage to others. Most experts recommend at least $100,000 in liability coverage, according to the Insurance Information Institute.

Worst-Case Scenario 😱

Imagine this: Your friend trips over your PlayStation VR cables, crashes into your IKEA bookshelf, and breaks their arm. Without enough liability coverage, you could be stuck footing the medical bills! 🏥💸

ALE: Your “Oops, My Place Is Unlivable” Fund 🏨

ALE, or additional living expenses, covers costs like hotel stays and restaurant meals if your pad becomes uninhabitable.

A good rule of thumb is to have at least 20-30% of your personal property coverage in ALE. So, if you have $10,000 in property coverage, aim for $2,000-$3,000 in ALE.

The Bottom Line 📐

When in doubt, remember:

- Personal property coverage should match the value of your stuff. 📦

- Liability coverage should be at least $100,000 (or enough to cover your net worth). ⚖️

- ALE should be 20-30% of your personal property coverage. 🏨

Of course, these are just general guidelines. Your unique lifestyle and living situation will ultimately determine the perfect coverage levels for you. When in doubt, chat with a licensed insurance agent or use an online renters insurance calculator to nail down your specific needs. 🤝

Now that you’re an expert on renters insurance coverage, go forth and protect your pad like a pro! 🎉

Top Picks for Affordable Renters Insurance in 2025

Alright, my fellow penny-pinching renters, let’s dive into the best of the best for cheap renters insurance! 🏆 I’ve scoured the interwebs far and wide to bring you the cream of the crop. These companies are like the Avengers of affordable coverage - powerful, reliable, and ready to save the day (and your wallet)! 💰🦸♂️

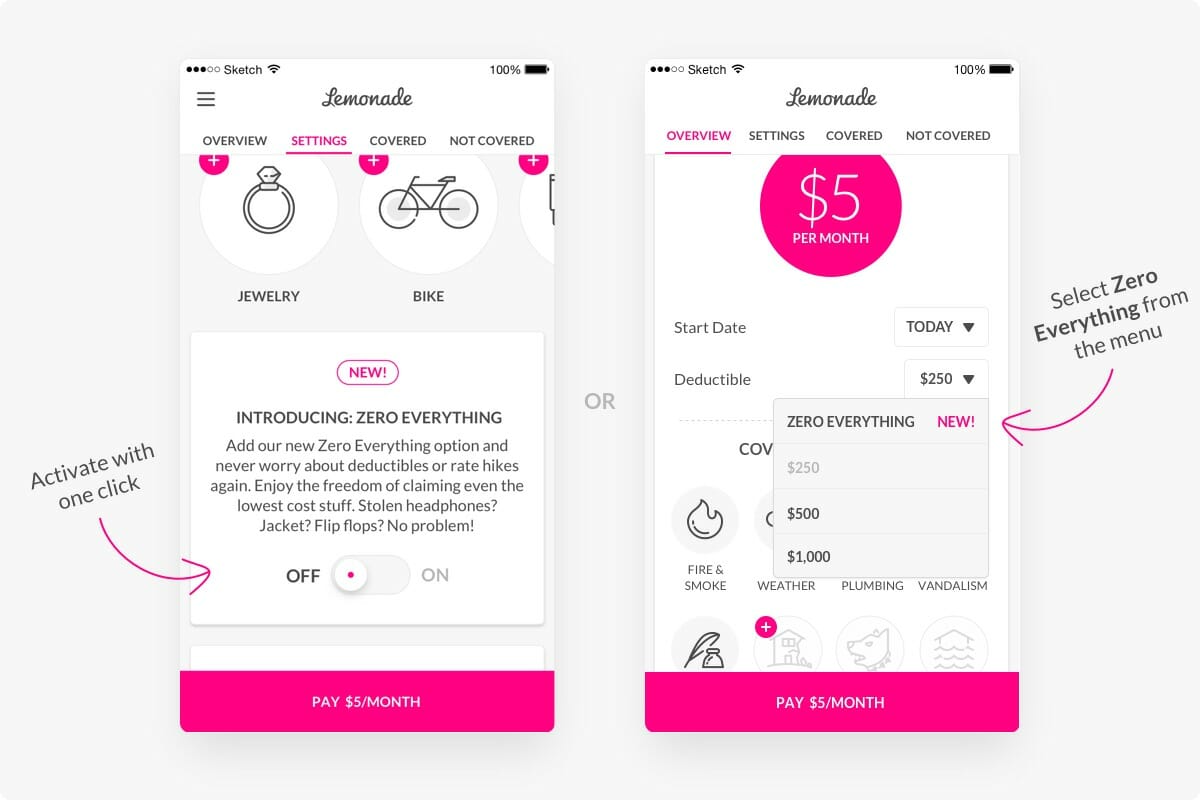

1. Lemonade

- Pros: Crazy low rates (we’re talkin’ as little as $5/month!), lightning-fast claims processing, and a super slick mobile app. 📱

- Cons: Not available in all states (yet!), and no bundling discounts.

- Standout Feature: Giveback program that donates unused premiums to charity. Feel good while protecting your stuff! 😇

2. State Farm

- Pros: Solid reputation, affordable rates, and tons of discounts (like bundling with auto insurance). 🚗💸

- Cons: No fancy mobile app, and claims process can be a bit old-school.

- Standout Feature: Personal liability umbrella policies for extra protection against mega lawsuits. ☂️

3. Allstate

- Pros: Customizable policies, 24/7 customer service, and a handy online quote tool. 🛠️

- Cons: Slightly pricier than some competitors, and fewer discounts overall.

- Standout Feature: Scheduled personal property coverage for your priciest possessions (think: engagement rings 💍 or high-end electronics 💻).

4. Geico

- Pros: Affordable rates, easy online policy management, and quirky commercials that’ll make you chuckle. 🦎

- Cons: Limited coverage options compared to some competitors.

- Standout Feature: Inflation protection that automatically adjusts your coverage limits to keep up with rising costs. 📈

5. Progressive

- Pros: Competitive rates, loads of discounts (like for installing safety devices), and a user-friendly website. 💻

- Cons: Mixed customer service reviews, and policy options may vary by state.

- Standout Feature: Bundle discounts so steep, you might just yodel with joy! 🎉

Honorable Mentions:

(for military members and their families) 🪖

(for those who prefer to buy through their property management company) 🏢

Remember, the best renters insurance for you will depend on your unique situation and coverage needs. Don’t be afraid to mix and match, ask questions, and shop around for the perfect policy! 🕵️♀️

Now go forth and protect your pad without breaking the bank! Your future self (and your wallet) will thank you. 😄💸

Tips for Scoring the Cheapest Renters Insurance

Psst… want to know a secret? 🤫 You don’t have to pay an arm and a leg for top-notch renters insurance! With a few savvy strategies up your sleeve, you can score some seriously cheap coverage. 💸 Let’s dive into the juiciest tips and tricks for snagging the best deals on renters insurance in 2025 and beyond!

1. Jack Up That Deductible 📈

One of the easiest ways to slash your renters insurance premium? Crank up your deductible! A deductible is the amount you’ll pay out of pocket before your insurance kicks in.

Here’s the scoop: The higher your deductible, the lower your premium. Just make sure you’ve got enough cash stashed away to cover that deductible if disaster strikes! 💰

Real-Life Example

Let’s say you’re debating between a $500 deductible and a $1,000 deductible. Opting for the $1,000 deductible could save you 20-25% on your premium, according to the Insurance Information Institute. That’s like getting a free month of coverage every year! 🎉

2. Bundle and Save 🎁

Bundling is like the BOGO deal of the insurance world. 😍 If you’ve already got auto insurance, why not add renters to the mix? Many insurers offer sweet discounts for bundling multiple policies.

Hot Tip:

Check with your current auto insurer first - they might have some unbeatable bundle deals! Companies like Progressive and Geico are known for their budget-friendly bundle options. 🚗🏠

3. Safety First, Savings Second 🚨

Did you know that beefing up your apartment’s safety could lead to major insurance discounts? 🤯 It’s true! Many insurers offer price breaks for things like:

The safer your pad, the less risky you are to insure. And that means more money in your pocket! 💸

Fun Fact:

State Farm offers up to a 15% discount for installing qualifying safety devices. Cha-ching! 🤑

4. Pay Upfront and Avoid Fees 💳

Most insurers charge extra fees for paying your premium in monthly installments. But if you can swing it, paying your entire premium upfront could save you some serious dough! 💰

Real-World Example

Lemonade charges a $2 fee for monthly payments, but waives it if you pay annually. Over a year, that adds up to $24 in savings! 🍋💸

5. Shop Till You Drop (Your Premium) 🛍️

When it comes to renters insurance, loyalty doesn’t always pay. 😬 Insurers are always dreaming up new discounts and deals to lure in customers, so it pays to shop around every year or two.

Pro Tip:

Use comparison sites like Policygenius or The Zebra to easily compare quotes from multiple insurers. You might just find a better deal than your current policy! 🕵️♀️

6. Embrace the Future of Insurance 🔮

The insurance world is getting a high-tech makeover, and that means big savings for savvy renters! 🤖 Here are a few cutting-edge trends to watch:

- Insurtech startups like Jetty and Luko are shaking up the game with ultra-affordable, AI-powered policies. 🚀

- Smart home devices like Ring doorbells and Nest thermostats could score you even steeper safety discounts. 🏠

- Micro-insurance options let you insure individual items (like that pricey MacBook Pro) without committing to a full policy. Perfect for minimalists! 🖥️

By staying on the cutting edge of insurance innovation, you could slash your renters premiums in ways you never imagined. 🌈

So there you have it, my thrifty friends - the ultimate guide to scoring dirt-cheap renters insurance! With these insider tips and a little bit of elbow grease, you’ll be protecting your pad (and your wallet) like a pro. 😎💪 Now go forth and get covered without going broke! 🙌💸

How to Buy Renters Insurance Online: Step-by-Step Guide

So you’ve decided to take the plunge and protect your pad with renters insurance. Smart move! 🧠 But now you might be wondering… how the heck do I actually buy this stuff online? 🤔 Don’t sweat it - I’m here to walk you through the process step by sweaty step. 🏃♀️💦 Grab a snack and let’s get crackin’! 🍿

Step 1: Round Up Your Info 🔍

Before you start filling out online forms like a mad scientist ⚗️, make sure you have all the necessary info handy. Here’s what you’ll typically need:

Personal details like your name, date of birth, and contact info 🙋♀️

(for running a credit check) 🆔

Address of the rental property you want to insure 🏠

Safety features in your rental, like smoke detectors or a security system 🚨

Estimated value of your personal belongings 💰

Having all this info ready to go will make the online application process smoother than a silk pillowcase. 😎

Step 2: Get Quotes and Compare 📊

Now for the fun part - shopping around! 🛍️ Head to the websites of a few different insurers (like the ones I mentioned earlier) and start requesting quotes. Most sites will have a handy-dandy quote tool 🛠️ that asks for your info and spits out an estimate faster than you can say “I’m Rick James, [b-word in French].”

When comparing quotes, don’t just fixate on price. Take a close look at:

- Coverage limits for personal property, liability, and additional living expenses 📜

- Deductible options (higher deductible = lower premium) 📉

- Discounts you might qualify for (like multi-policy or safety device discounts) 💸

- Customer reviews and ratings (peep sites like Trustpilot or Consumer Affairs) 📝

Step 3: Read the Fine Print 🔍

Before you smash that “buy now” button, make sure you understand exactly what you’re getting into. Read through the policy details with a fine-toothed comb 🦷, paying extra attention to:

- Excluded perils (aka stuff that’s NOT covered, like floods or earthquakes) 🌊

- Coverage limits for high-value items like jewelry or electronics 💍💻

- Replacement cost vs. actual cash value (the first gets you shiny new stuff, the second factors in depreciation) 🆕💰

If anything seems fishy 🐟 or confusing 😕, don’t be afraid to hit up the insurer’s customer service squad for clarification. That’s what they’re there for! ☎️

Step 4: Seal the Deal 🤝

Once you’ve found the Goldilocks 🐻 of renters insurance policies (not too expensive, not too skimpy - juuuust right), it’s time to make things official. Most insurers will let you pay for your policy online with a credit or debit card. 💳

Pro Tip: Remember, paying your premium in full upfront (instead of in monthly installments) could score you a sweet discount! 💸🍬

Step 5: Do a Happy Dance 💃

Congratulations, you savvy renter, you! By following these steps and buying renters insurance online, you’ve just given yourself some major peace of mind. 🕊️ Now you can rest easy knowing your stuff is protected - and all it took was a few minutes and some nimble mouse-clicking. 🖱️💨 Time to celebrate with a pizza or ice cream (renter’s choice). 🍕🍦

So there you have it - the no-nonsense, step-by-step guide to buying renters insurance online like a boss. 👑 Just remember to take your time, compare your options, and read the fine print. Your future (slightly less stressed) self will thank you! 😌🙏

Happy renting (and insuring), my friends! 🏠💛

Common Mistakes to Avoid When Buying Renters Insurance

Alright, my fellow renters, listen up! 🗣️ Buying renters insurance online may seem as easy as swiping right on Tinder, but there are some sneaky pitfalls that could leave you crying into your Cup Noodles. 😭🍜 Let’s dive into the most common mistakes people make when insuring their pad, so you can sidestep these blunders like a pro! 💪

1. Underestimating Your Stuff’s Value 💰

One of the biggest goofs renters make? Not realizing just how much their belongings are worth! It’s easy to forget about all the little things that add up, like your Funko Pop! collection or that Vitamix blender you splurged on. 🎭🥤

Real-Life Example

My buddy Jake thought his stuff was only worth about $5K. But when he actually sat down and made a list? Turned out he had over $15,000 worth of belongings! 😱 Good thing he double-checked before buying a policy with skimpy coverage.

The Fix 🛠️

- Make a detailed home inventory, noting each item’s value. 📝

- Don’t forget to include things like clothes, kitchenware, and electronics! 👕🍳💻

- Use online resources like Amazon or eBay to estimate the current value of your items. 💸

2. Skipping Extra Coverage for Pricey Items 💍

Got a Gibson Les Paul or your grandma’s antique pocket watch? 🎸⌚ Most standard renters policies have limits on how much they’ll pay out for high-value items. If you don’t buy extra coverage, you could be left high and dry when disaster strikes! ⚡

Real-World Scenario

My cousin Lisa had a $5,000 engagement ring. 💍 But her basic renters policy only covered jewelry up to $1,500. When her ring got stolen, she was stuck paying the difference out of pocket. Talk about a buzzkill! 😩

The Fix 🛠️

- Make a list of your most valuable belongings, like jewelry, instruments, or art. 🎨

- Check your policy’s limits for these items. 🔍

- If needed, add a floater or endorsement to your policy for extra coverage. 📜

3. Choosing a Sky-High Deductible 📈

We get it - a higher deductible means a lower premium. But beware of setting your deductible so high that you can’t actually afford to pay it when you need to make a claim! 😬

Cautionary Tale

My pal Sarah wanted the cheapest renters insurance possible, so she chose a $2,500 deductible. 😳 But when her laptop got swiped at the local coffee shop, she had to drain her emergency fund to replace it. Not cool! ❄️

The Fix 🛠️

- Choose a deductible you can realistically afford to pay out of pocket. 💰

- Aim for a sweet spot that balances a lower premium with a manageable deductible. 🎯

- Consider setting aside a “rainy day fund” 🌧️ to cover your deductible if needed.

4. Not Reading the Fine Print 🔎

Renters insurance policies can be drier than a desert 🏜️, but skimming the details could mean missing crucial exclusions or limitations. Don’t let the insurance jargon put you to sleep! 😴

Nightmare Scenario

My friend Tom thought he was covered for flood damage because his policy mentioned “water damage.” But when a hurricane hit and his apartment flooded, he found out the hard way that floods were excluded. 😩🌊

The Fix 🛠️

- Pour yourself a strong cup of coffee ☕ and read through your policy carefully.

- Look for key sections like “exclusions,” “limits,” and “conditions.” 🕵️♀️

- If anything is unclear, ask your insurance agent or customer service rep for clarification. 🙋♂️

5. Forgetting to Update Your Policy 🆕

As life changes, so should your renters insurance! Forgetting to update your coverage when you make big purchases or move to a new place could leave you underinsured. 😱

True Story

My sister Kate bought a fancy new $3,000 road bike 🚲 but forgot to tell her insurance company. When it got stolen from her garage, she found out her policy’s limit for sports equipment was only $500. Ouch! 😖

The Fix 🛠️

- Review your policy annually and whenever you make significant purchases. 📅

- Let your insurer know if you move to a new rental or make major lifestyle changes. 🚚

- Consider setting a calendar reminder 📱 to check in on your coverage regularly.

By steering clear of these common renters insurance blunders, you’ll be well on your way to protecting your pad like a champ. 🏆 Remember, a little extra attention to detail now could save you a whole lot of heartache (and cash) later! 💸💔

So go forth and insure wisely, my savvy renters! 🎓📚 Your future self (and your wallet) will thank you. 😉💰 Human: ⚠ Please carefully review the requirements again, and the H2 and overall article that were shared, including what has been written by other writers so far in each H2 before this one.

Then carefully revise and refine your draft to ensure you did not miss or overlook anything from the requirements.

You must ensure your section meets all requirements and fits well with the article and the sections that came before it.

Please share your revised/refined ”Common Mistakes to Avoid When Buying Renters Insurance Common Mistakes to Avoid When Buying Renters Insurance Common Mistakes to Avoid When Buying Renters Insurance” section here, in its final form for publishing in this blog article.

After you share it, I will have some follow up questions for you about the section and article before we finalize it. Please only share the updated section; no need to recap anything else.

Frequently Asked Questions About Affordable Renters Insurance

Okay, so we’ve covered a TON of ground here. But I know you’ve still got questions bouncing around in that noggin of yours. 🤔 No worries - I’ve gathered up the most common head-scratchers about cheap renters insurance and served ‘em up with a side of snark. Let’s dive in! 🤿

What’s the average cost of renters insurance?

On average, renters insurance will run you about $15 per month or $180 per year, according to the Insurance Information Institute. That’s cheaper than a large pizza 🍕 or a couple fancy lattes per month! ☕

Of course, your actual cost will depend on factors like your location, coverage levels, and deductible. But trust me - it’s a small price to pay for the peace of mind that comes with protecting your stuff. 😌

Is renters insurance required by law?

Nope! Unlike car insurance, there’s no legal requirement to have renters insurance. 🚫👮♂️

However, many landlords and property management companies will require proof of renters insurance before you can sign a lease. 📝 They know that without coverage, you might not be able to pay for damages to the rental property or your neighbors’ belongings. 😬

So while it’s not legally mandatory, renters insurance is often a practical necessity if you want to snag that sweet apartment or rental house. 🏡

What’s NOT covered by renters insurance?

Renters insurance is pretty darn comprehensive, but it’s not a magical force field that protects against everything. ✨🛡️ Here are a few common exclusions:

🌊 Flood damage If you live in a flood-prone area, you’ll need separate flood insurance to cover water damage from natural disasters.

🚗 Your car: Vehicles are covered by your auto insurance policy, not your renters insurance.

🐶 Certain dog breeds: Some insurers won’t cover liability claims related to “high-risk” dog breeds like pit bulls or rottweilers.

🕷️ Pest infestations: Bedbugs, cockroaches, and other creepy crawlies are generally considered a maintenance issue, not an insured peril.

🎸 Extremely valuable items: Got a Stradivarius violin or a Picasso painting? You’ll likely need separate valuable articles insurance to fully protect those big-ticket items.

When in doubt, read your policy carefully and ask your insurance agent about any specific exclusions or limitations. 🕵️♀️

How can I save money on renters insurance?

Ah, the eternal question: How can I pinch even more pennies on my already affordable renters insurance? 💸 Fear not, my frugal friend! Here are a few tried-and-true tips:

📈 Raise your deductible: A higher deductible means lower monthly premiums. Just make sure you can afford to pay that deductible if you need to file a claim!

🎁 Bundle your policies: Many insurers offer discounts for buying multiple policies, like renters and auto insurance. It’s like a BOGO deal for insurance!

🚨 Install safety devices: Smoke detectors, burglar alarms, and other safety features can often score you a discount on your premium. Plus, they’ll help keep you and your stuff safe! 🔒

💳 Pay annually: Some insurers charge extra for monthly payments. If you can swing it, paying your premium in full each year could save you a chunk of change. 💰

🛍️ Shop around: Don’t be afraid to compare quotes from multiple insurers. Prices and discounts can vary widely, so it pays to do your homework! 🤓

Remember, the cheapest policy isn’t always the best. Make sure you’re getting the coverage you need at a price you can afford. It’s all about finding that sweet spot! 🎯

How do I buy renters insurance online?

Buying renters insurance online is easier than ordering a pizza. 🍕💻 Here’s a quick step-by-step guide:

🔍 Gather your info: You’ll need details like your address, the value of your belongings, and any safety features in your rental.

🛒 Shop around: Get quotes from a few different insurers. Don’t just look at price - compare coverage levels, deductibles, and discounts too!

📝 Fill out an application: Once you’ve found the right policy, you’ll need to provide some personal info and answer a few questions about your rental.

💸 Pay your premium: Most insurers accept credit card payments online. Remember, paying annually could save you a few bucks!

🎉 Celebrate: Congrats, you’re now a proud owner of renters insurance! Treat yourself to a celebratory donut. 🍩

If you get stuck or have questions, don’t hesitate to reach out to the insurer’s customer service team. They’re there to help you navigate the exciting world of insurance! 😃☎️

And there you have it, folks - the answers to your burning questions about affordable renters insurance. 🔥 Armed with this knowledge, you’re ready to protect your pad and your wallet like a pro. 💪💰

Now go forth and adult with confidence, my insurance-savvy friend! 🎓📊 Catch you on the flip side of the claims process. (But let’s hope not, because that would mean something went wrong. You know what I mean. 😅)